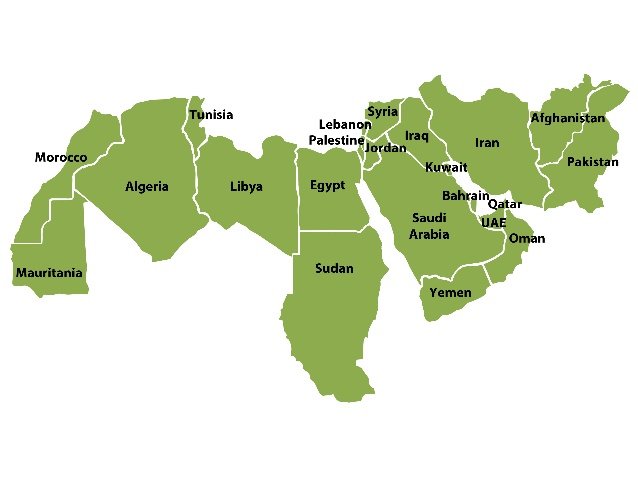

The World Bank has begun classifying Pakistan within a newly expanded regional framework: MENAAP, Middle East, North Africa, Afghanistan, and Pakistan. Introduced in the Bank’s FY2026 regional economic updates and publications, the framework places Pakistan alongside economies stretching from the Gulf to North Africa, including Saudi Arabia, the UAE, Egypt, Jordan, and Tunisia.

For decades, Pakistan was analytically grouped within South Asia alongside India, Bangladesh, Sri Lanka, Nepal, Bhutan, and the Maldives. The emergence of MENAAP signals a notable change in how major international financial institutions increasingly interpret Pakistan’s economic orientation and development profile.

Although the World Bank has described the framework largely in administrative and analytical terms, such classifications often shape how countries are benchmarked, financed, and understood within global development discourse. For Pakistan, a country of more than 240 million people facing persistent fiscal pressures, energy insecurity, and structural reform challenges the shift carries both symbolic and strategic significance.

What is MENAAP?

The concept itself is not entirely new. The International Monetary Fund (IMF) has long used the MENAP grouping Middle East, North Africa, Afghanistan, and Pakistan in its regional economic reporting and analysis. The World Bank’s adoption of a similar MENAAP framework therefore reflects an emerging institutional alignment among major multilateral organisations.

While Pakistan remains geographically part of South Asia, the framework acknowledges the country’s increasingly westward economic orientation. Analysts note that Pakistan’s strongest economic linkages today are tied less to South Asian trade integration and more to Gulf labour markets, remittance inflows, energy dependencies, and investment partnerships.

Pakistan also becomes one of the largest population centres within the grouping, giving it significant demographic weight within the wider MENAAP framework.

Why Did the Shift Happen?

Although the World Bank has not publicly framed the move in geopolitical terms, many economists and regional analysts view it as recognition of Pakistan’s evolving economic realities.

The clearest example is Pakistan’s remittance-driven external sector. According to State Bank of Pakistan data, remittances remain among the country’s largest sources of non-debt external inflows, consistently exceeding foreign direct investment. A substantial share originates from Gulf Cooperation Council (GCC) states, particularly Saudi Arabia and the UAE.

Pakistan’s economy also shares several structural characteristics commonly seen across MENA economies, including:

- dependence on energy imports,

- high youth unemployment pressures,

- rapid population growth,

- vulnerability to external financing shocks, and reliance on sovereign or state-backed investment flows

Analysts argue that grouping Pakistan with economies facing comparable structural challenges may allow for more relevant policy comparisons than benchmarking it exclusively against rapidly industrialising South Asian economies such as India and Bangladesh.

Breaking Away from the South Asian Frame

For decades, Pakistan’s economic story within South Asia was frequently framed in comparison with India. However, regional economic integration within South Asia has remained limited due to longstanding geopolitical tensions, while SAARC has struggled to maintain meaningful momentum.

At the same time, Pakistan’s diplomatic and economic engagement has increasingly deepened with Gulf states. Saudi Arabia and the UAE remain among Pakistan’s most important bilateral economic partners through deposits, investment commitments, energy cooperation, and labour-market linkages.

The long-discussed Pakistan-GCC Free Trade Agreement negotiations further reflect Islamabad’s growing emphasis on westward economic connectivity. Observers suggest that the World Bank’s adoption of the MENAAP framework formalises trends policymakers and economists have recognised for years: Pakistan’s economic centre of gravity has steadily shifted toward the Gulf and wider Middle East.

Strategic Implications

The significance of this reclassification extends beyond terminology.

First, the shift changes the comparative lens through which Pakistan’s economic performance may increasingly be assessed. Instead of being measured primarily against some of Asia’s fastest-growing economies, Pakistan may now be analysed alongside countries such as Egypt, Jordan, or Tunisia, economies facing similarly complex structural and fiscal constraints.

Second, the reclassification could influence how development institutions frame policy recommendations related to labour markets, energy transition, youth employment, and private-sector reform. Analysts argue that Pakistan’s developmental profile often resembles several MENA economies more closely than export-driven South Asian manufacturing economies.

Third, the symbolism itself matters. Regional classifications help shape investor narratives and institutional perceptions. Inclusion within a broader MENA-linked framework may strengthen Pakistan’s positioning within Gulf-centred investment and financial networks, particularly as Gulf sovereign wealth funds expand their economic footprint across emerging markets.

Potential Economic Opportunities

Supporters of the shift argue that closer institutional alignment with MENA economies could create several opportunities for Pakistan.

One potential benefit lies in attracting greater Gulf investment. Saudi Arabia, the UAE, and Qatar have increasingly signalled interest in sectors such as mining, infrastructure, energy, logistics, agriculture, and technology within Pakistan.

Pakistan’s growing technology sector may also benefit from stronger integration with Gulf markets. Pakistani IT exports have expanded steadily in recent years, while several local firms have increased their presence in Saudi Arabia and the UAE. Industry observers believe institutional alignment with the MENA framework could improve business confidence and market access for Pakistani firms seeking regional expansion.

Similarly, deeper integration with Gulf economies may improve prospects for labour mobility, digital services exports, and long-term investment partnerships.

Risks and Challenges

The shift, however, is not without risks.

The broader MENA region remains vulnerable to geopolitical instability, conflict spillovers, and energy market disruptions. Escalating tensions in West Asia including concerns surrounding shipping routes and oil supply chains directly affect Pakistan due to its heavy dependence on imported energy.

Critics also caution that moving away from the South Asian growth narrative may carry reputational downsides. South Asia remains among the world’s fastest-growing economic regions, whereas several MENA economies continue to struggle with debt pressures, political instability, and slow growth.

Some analysts further argue that changing Pakistan’s institutional peer group could reduce external pressure for competitiveness and reform relative to high-performing Asian economies.

Additionally, because different multilateral organisations continue to use varying regional frameworks, the transition may create inconsistencies in comparative development analysis and regional programming.

Looking Forward

Pakistan’s inclusion within the World Bank’s MENAAP framework represents less a sudden geopolitical shift than a formal acknowledgement of trends that have developed over many years.

Pakistan’s largest remittance flows originate from the Gulf. Its most influential bilateral economic relationships increasingly involve Saudi Arabia and the UAE. Its energy security, labour exports, investment partnerships, and external financing needs are deeply tied to the broader Middle East

Regional classifications do more than organise data, they shape how nations are perceived, benchmarked, and financed.

For supporters, the framework offers opportunities for deeper Gulf investment integration, more tailored development analysis, and stronger positioning within emerging MENA economic networks. For critics, it risks embedding Pakistan within a region frequently associated with instability and economic volatility.

Ultimately, the reclassification itself does not alter Pakistan’s economic fundamentals. It reflects how international institutions are increasingly interpreting Pakistan’s place within the global economic landscape. Whether the shift proves beneficial will depend less on institutional labels and more on Pakistan’s ability to pursue sustainable reforms, strengthen competitiveness, and translate regional connectivity into long-term economic gains.